How We Invest

Your investments, your tax strategy, and your life stage should all be working together. Here's how we make that happen.

We're methodical about how we build portfolios, how we manage the tax consequences, and how we adapt as your life changes.

1. How we build the portfolio.

We take the investment side seriously. Every portfolio we build starts from a set of principles that's been tested against decades of market data. Here's what we believe and how it translates into your portfolio.

We diversify globally. Different regions of the world take turns leading in stock market performance. International and emerging market stocks outpaced U.S. stocks for much of the 2000s. Then U.S. stocks dominated the 2010s and early 2020s. The leader rotates, and there's no reliable way to predict when. So we build blended allocations across U.S., international, and emerging market stocks to make sure you're positioned wherever the next opportunity shows up.

We use low-cost, passively managed investments for most of the portfolio. Data shows that the vast majority of funds failed to beat a basic index fund over the prior decade, after fees. The evidence is clear: capturing the market return at a low cost beats paying someone to try to outguess it.

We don't try to time the market, and we'd caution you against it too. Here's something you can count on: you'll be fed compelling investment narratives for the rest of your life. A headline warns that a crash is coming. A CNBC guest says to get out now, or to go all in on whatever's been working lately. These stories sound smart in the moment, and they tempt you into believing this time is different. The data says otherwise. There's almost no evidence that anyone can reliably time the market. For every correct call someone makes, they tend to make just as many wrong ones, and the wrong ones are expensive.

So we hold through the ups and downs in a disciplined, structured way and capture the return the market delivers over time. Put simply, being an average investor is a great outcome for the vast majority of people. What we can't afford is to be below-average investors. And trying to outguess the market is one of the most reliable ways to end up below average. The chart below makes this concrete. Over a multi-decade horizon (as measured below by JP Morgan), the "average investor" earned far less than a basic portfolio, not because they picked bad investments, but because of the behavior around them: buying high, selling low, and chasing whatever was hot at the time.

We often hold a basket of hedges alongside stocks. These include inflation-protected Treasury bonds (which adjust with the cost of living), broad commodity funds (which own raw materials like oil, metals, and agricultural products), real estate investment trusts, and long-term government bonds. Each one responds differently to shifts in economic growth and inflation. When properly diversifying your portfolio, you ideally should seek an outcome when one part of the portfolio gets hit, another tends to hold up or rise. This gives us something to sell at a gain and redeploy into the beaten-down asset. That's the actual mechanics behind "buy low, sell high."

Our view is that changes in growth expectations and inflation expectations are the two forces that drive investment returns over time. When growth expectations rise, stocks tend to do well. When inflation spikes unexpectedly, inflation-protected bonds and commodities tend to hold up better, while traditional stocks and bonds typically don't. When growth expectations fall, bonds often rally as investors seek safety. We build portfolios with these scenarios in mind, not portfolios that depend on one particular outcome.

2. How we manage the taxes around the portfolio.

Two people can hold the exact same investments and end up with very different results after taxes. The difference often comes down to which investments sit in which accounts, whether anyone is paying attention to the tax consequences, and how disciplined the ongoing management is. These details compound year after year. Over a 20- or 30-year time horizon, the gap can be enormous.

We place investments in accounts based on their tax characteristics. Investments that generate a lot of taxable income each year (like bonds and real estate funds) tend to go inside tax-sheltered accounts such as your 401(k) or IRA, where that income can grow tax-deferred until withdrawal. Investments with low turnover and favorable tax treatment (like broad stock index funds) generally go in your taxable brokerage account, where they can grow with minimal annual tax drag. This is straightforward in concept but routinely overlooked, and the cost of neglecting it accumulates over decades.

We look for tax loss harvesting opportunities. When an investment drops below what you paid for it, we can sell it to capture the loss, immediately replace it with a similar investment to maintain your market exposure, and use that loss to offset gains elsewhere or reduce your taxable income. This is a discipline, not a one-time event, and the benefit compounds over time.

When a new client brings us an existing portfolio, we don't tear it down on day one. If your investments have gained significantly, selling everything to build a new allocation would hand the IRS a capital gains bill that might take years to recover from. We assess the tax cost and build a transition plan that moves you toward your target allocation over time, using new contributions, and rebalancing opportunities to get there without triggering unnecessary taxes.

3. How the system adapts to where you are in life.

The principles don't change. But a 35-year-old with stock options vesting every quarter and a 63-year-old two years from retirement need very different portfolio structures, different account priorities, and different planning around every move. Here's how we adapt.

Building Wealth Phase

You're earning well. Every dollar needs a job, and most of yours don't have one yet.

You have RSUs vesting, maybe an ESPP, maybe stock options on top of your salary. Your 401(k) is growing. Cash is sitting in a savings account. You know you should be doing more with it, but the complexity keeps you from acting.

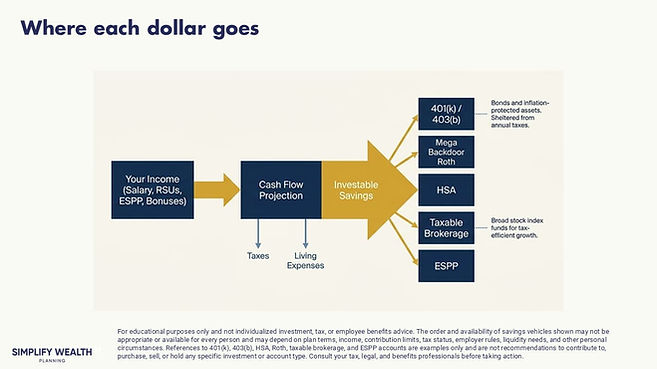

We start with your cash flow. Income in, taxes out, spending accounted for. From there, we route each dollar to the right place. Mega backdoor Roth available in your 401(k) plan? We consider using it. ESPP discount on the table? We help you decide how to handle the shares once they vest. Deferred compensation offered and you're in a top bracket? We run the trade-offs. Then we place each investment in the account type where it's most tax-efficient, following the asset location principles from Section 2.

The portfolio itself is globally diversified and low-cost. What makes it personal is the tax architecture wrapped around it and the coordination with your compensation.

Approaching Retirement Phase

You're 3 to 7 years out. The portfolio needs to start changing shape.

You might be sitting on a concentrated stock position from years of employer stock awards. You've been reluctant to sell because of the tax hit, so the position has grown into an outsized share of your net worth. You might also have a gap between when you plan to stop working and when you can access retirement accounts penalty-free at 59 and a half.

This is the window where we start repositioning. We build a plan to diversify concentrated holdings over time. We consider shifting the investments you'll need in the first few years of retirement into lower-volatility, income-oriented positions so that money is stable and accessible when you need it. And we start planning the bridge, making sure you'll have access to cash flow in those early retirement years before your retirement accounts open up.

For people in a transition period, this doesn't often happen as a single event. It's usually a sequence of moves over several years, timed to your income, your tax brackets, and your retirement date.

Living Off Your Portfolio Phase

Retirement income isn't one-size-fits-all. How you're wired matters as much as the math.

There's a critical question that needs to be answered: how do you actually feel about risk when your paycheck stops? Some people are comfortable with a systematic withdrawal strategy from a diversified portfolio, adjusting spending as the market moves up and down. Others can't sleep unless they know a baseline income is guaranteed no matter what happens. These aren't right-or-wrong answers. They're personality differences, and they lead to very different portfolio designs.

We have every retirement client take a formal retirement income style assessment before we build anything. The assessment maps where you fall along two dimensions: whether you lean toward probability-based strategies (staying invested in the market and adjusting as you go) or safety-first strategies (locking in guaranteed income). Your answers shape the structure of everything that follows.

For a client who's comfortable staying invested and wants maximum flexibility, we might use a systematic withdrawal approach with dynamic spending guardrails. What that means is you draw from a diversified portfolio, and if the portfolio rises above a defined threshold, your spending can increase by a set amount. If it falls below another threshold, spending gets trimmed by a set amount. The adjustments are small, predictable, and agreed on in advance, so you're never guessing whether you can afford the trip or the home project.

For a client who needs more certainty, we might pair a guaranteed income floor (through something like a bond ladder designed to cover essential expenses) with a growth-oriented portfolio for everything above that floor. You know your baseline is covered regardless of what the market does, and the rest of your money stays invested with a longer time horizon.