How to Harvest Capital Gains in the 0% Tax Bracket During Retirement

- Marcel Miu, CFA, CFP®

- Apr 23

- 8 min read

TL;DR

Tax-gain harvesting lets retirees with low taxable income sell appreciated investments and pay zero federal capital gains tax. Since wash sale rules apply only to losses, investors can buy back the same asset minutes later and reset the cost basis higher. This often saves money on future taxes.

The Free Lunch in the Tax Code

Sarah and Mark retired at age sixty. They live off their investments. Their taxable income dropped to nearly zero. A taxable brokerage account they own grew by $80,000 over the last few years. The couple decided against letting that embedded tax liability sit there. Hitting the reset button made sense. They sold the assets. Paying zero federal tax on the gain was a huge win, and buying the assets right back secured their market position.

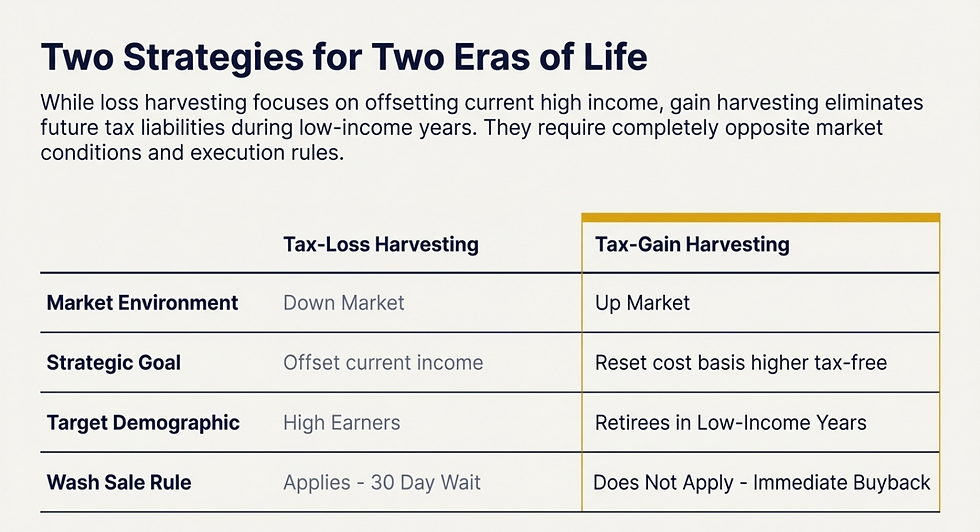

Retirees often focus on tax-loss harvesting to offset gains. But many miss the massive opportunity hidden in low-income years. Washing away future tax bills requires proactive planning. Harvesting gains demands careful calculation of your total income.

Most people spend their working years avoiding capital gains taxes. High salaries push them into the highest tax brackets. The government takes a large cut every time they sell a profitable stock. Retirement changes the math, though. Stopping work means your earned income drops and the tax code treats you in a new way. The 0% long-term capital gains bracket becomes available for many and can be used to save money over the long run.

*Market conditions do not guarantee a profit or protect against a loss

What Exactly Is Tax-Gain Harvesting?

Selling appreciated assets in a taxable account realizes a long-term capital gain (assuming you hold over 1 year). Paying a 0% federal tax rate on the profit is the primary goal. You then repurchase the asset to establish a higher cost basis.

This is different than tax-loss harvesting, which is used to offset gains elsewhere. The goal of gain harvesting is to reduce (or eliminate in some cases) future tax liabilities. Both strategies require discipline and a thorough understanding of your tax picture.

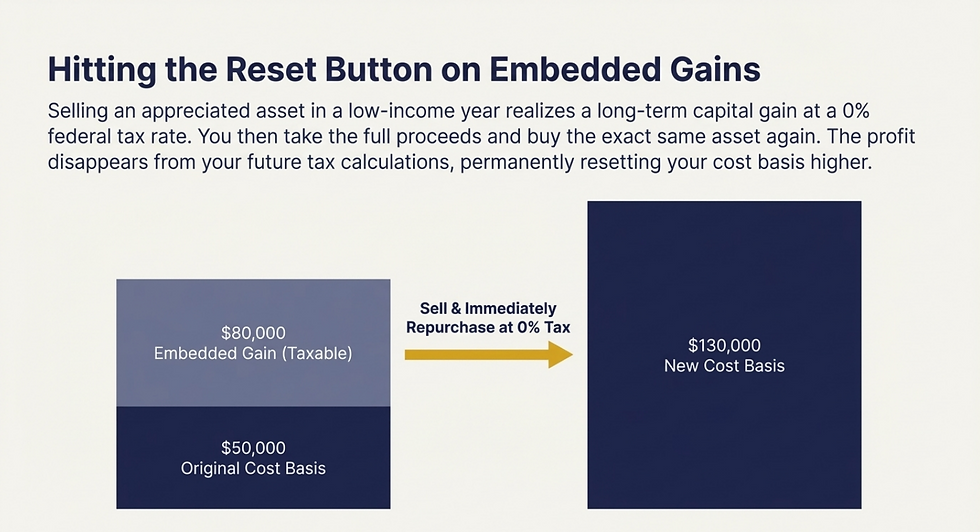

Let's look at the cost basis. Cost basis is the original price you paid for an investment. Buying shares of a fund for $50,000 sets your basis at $50,000. Ten years later, that fund might be worth $130,000. You have an $80,000 embedded gain. Selling the fund triggers taxes on that $80,000.

Gain harvesting can change the outcome. You sell the fund when your income is low (in this case, while still in the 0% long-term capital gains bracket). The IRS taxes the $80,000 gain at 0%. You take the entire $130,000 and buy the same fund again. Your new cost basis is $130,000. The $80,000 gain disappears from your future tax calculations.

*Investing involves risk. The value of your newly purchased fund will fluctuate.

How Do You Qualify for the 0% Capital Gains Bracket?

The 0% bracket applies to long-term capital gains and qualified dividends. You must hold the asset for more than one year to qualify. Shorter holding periods are considered short-term capital gains, which the IRS taxes at your ordinary income tax rates (which are usually higher).

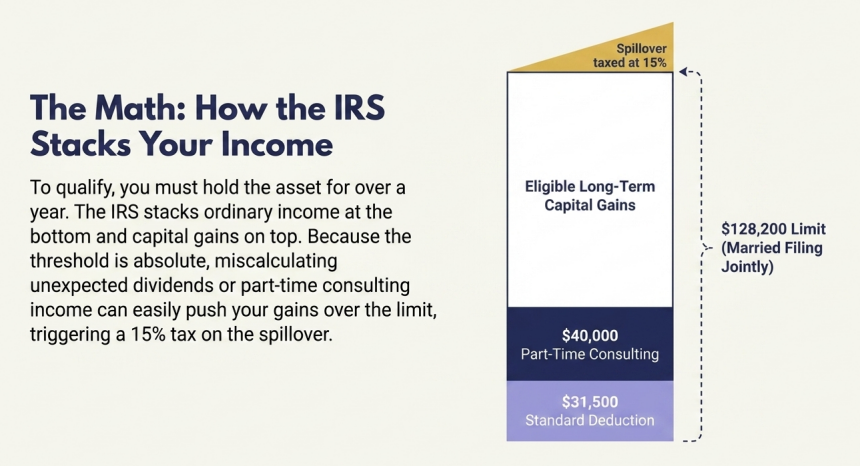

To find your 0% limit, you add your standard deduction to the top end of the 0% capital gains bracket. For example, in 2025, a married couple filing jointly can have up to $128,200 of Gross Income (a $31,500 standard deduction + the $96,700 capital gains bracket limit) before paying federal capital gains tax. This threshold changes every year with inflation, so be sure to check the current IRS limits.

Ordinary income sits at the bottom of your tax calculation. Capital gains sit on top. The IRS stacks your money to determine your rate. Earning an unexpected bonus, withdrawing from a traditional IRA, or receiving non-qualified dividends increases your ordinary income at the bottom. This can push your capital gains at the top over the line, triggering a 15% or 20% tax on the overflowing gains.

Let's walk through an example using 2025 numbers. John and Jane are married filing jointly, giving them a standard deduction of $31,500. They earn $40,000 in ordinary income from part-time consulting. Their standard deduction completely absorbs the first $31,500, leaving them with just $8,500 of Taxable Ordinary Income sitting at the bottom of their bucket. Because the 2025 0% capital gains bracket goes up to $96,700, they still have $88,200 of space remaining ($96,700 limit - $8,500 ordinary income). They can harvest up to $88,200 in long-term capital gains without paying a single dollar in federal capital gains tax.

*This strategy requires precise execution. Miscalculating your income could push your gains into the 15% bracket.

Why Do Wash Sale Rules Not Apply to Gains?

Investors assume they must wait 30 days to buy back a sold asset. The IRS wash sale rule applies only to capital losses. It prevents people from faking a loss to lower their tax bill. The IRS permits you to realize a gain whenever you want. Recognizing taxable income never bothers the government.

You can sell an index fund at a gain in the morning and buy it back minutes later. This immediate repurchase sets gain harvesting apart from loss harvesting. Loss harvesting forces you to buy a different asset. You must wait 31 days to buy back the original asset. Gain harvesting has no restrictions. The freedom to trade immediately reduces your time out of the market. Time out of the market can result in missed growth.

*Past performance does not guarantee future results.

How Do Roth Conversions Interfere With Gain Harvesting?

Early retirees often use low-income years to convert pre-tax IRA money to a Roth IRA. These conversions move money from a taxable environment to a tax-free environment. Roth conversions generate ordinary income. That ordinary income eats up the space in the 0% capital gains bracket.

We help calculate whether converting IRA funds at lower ordinary income rates makes more sense than harvesting gains at 0%. Prioritizing one strategy often means sacrificing the benefits of the other.

Every dollar you convert to a Roth IRA fills up your tax bucket from the bottom. Harvesting a dollar of capital gain fills up the bucket from the top. Doing both at the same time usually results in a tax bill. A financial plan helps you decide which strategy provides a greater long-term benefit. Tax laws change and the strategy that works today might not work next year.

Navigating the Ripple Effects

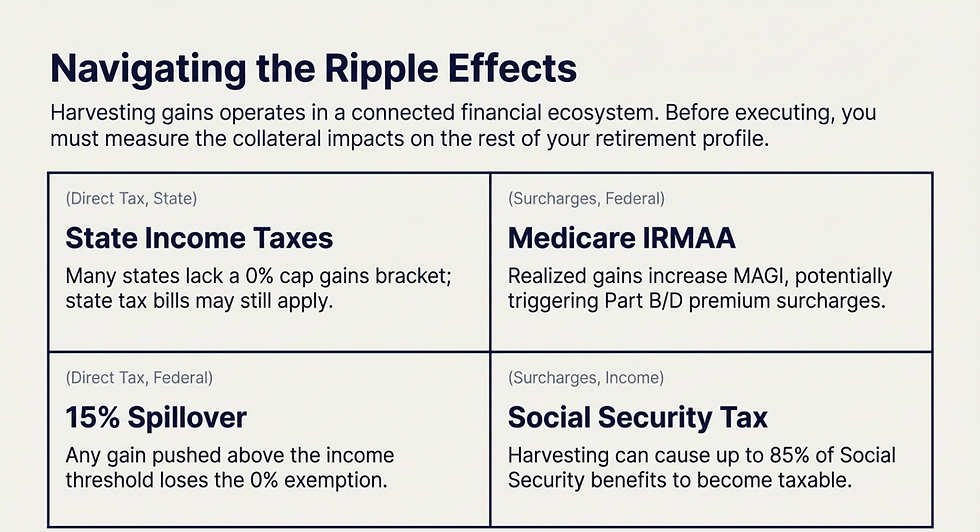

Harvesting gains operates in a connected financial ecosystem. Before executing any trades, you must measure the collateral impacts on the rest of your retirement profile. We look at four specific areas to ensure the strategy makes sense.

State income taxes matter. Many states don't have a zero percent capital gains bracket. Harvesting gains federal tax-free might still generate a state tax bill. You have to calculate the net benefit.

Medicare premiums can increase. Realized gains increase your Modified Adjusted Gross Income. Higher income can trigger IRMAA surcharges. These surcharges increase your Medicare Part B and Part D costs.

Social Security benefits might face taxes. Realized gains increase your combined income. Up to eighty-five percent of your benefits can become taxable if your income rises too high.

Pushing past the limit triggers the fifteen percent bracket. Any gain pushed above the income threshold loses the zero percent exemption. Careful planning keeps your gains within the tax-free zone.

Key Takeaways

The 0% capital gains bracket is a powerful tool for early retirees. Living off cash or principal makes this strategy possible. You must hold the asset for over a year to qualify for long-term capital gains rates. Holding periods carry market risk.

Wash sale rules do not apply to gains. You can buy the asset right back without a waiting period.

And watch out for state taxes. Some states tax capital gains as ordinary income. Executing this strategy in a high-tax state might erase the federal benefits.

FAQs

Are qualified dividends included in the zero percent bracket?

Yes. Qualified dividends and long-term capital gains share the same tax thresholds. Earning qualified dividends fills up your zero percent bucket alongside your harvested gains.

Does harvesting gains affect my mutual fund distributions?

No. Gain harvesting resets your cost basis. It doesn't change how the mutual fund distributes internal capital gains or dividends at the end of the year.

Can I harvest gains if only one spouse is retired?

Yes. The IRS looks at your combined income for married couples filing jointly. You can harvest gains as long as your total household income stays under the threshold.

Your Next Steps

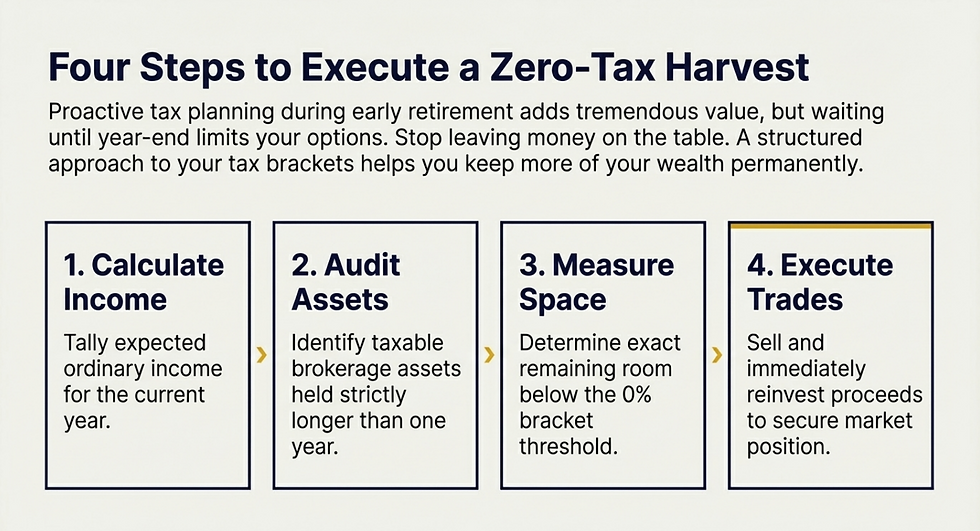

Stop Leaving Money on the Table

Proactive tax planning during early retirement adds tremendous value. Waiting until the end of the year limits your options. A structured approach helps you keep more of your wealth.

If you would like to learn more about our financial planning process and discuss whether our services are right for your financial objectives, feel free to schedule a consultation with our team.

To learn more about how we partner with clients, click here to view our services.

This blog is for educational purposes only and should not be taken as individual advice

Simplify Wealth Planning

Fast-Tracking Work Optional For Employees Earning Company Stock | Turn Your Stock Comp Into Wealth, Cut Taxes & Live Life Your Way | Flat Fees Starting at $8,000

Marcel Miu, CFA and CFP®, is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping employees earning company stock master their money and achieve their financial goals.

Disclosures

Simplify Wealth Planning, LLC (“SWP”) is a registered investment adviser in Texas and in other jurisdictions where exempt; registration does not imply a certain level of skill or training.

If this blog refers to any client scenario, case study, projection, or other illustrative figure, such examples are hypothetical and based on composite client situations. Results are for informational purposes only, are not guarantees of future outcomes, and rely on assumptions specific to the scenario (e.g., age, time horizon, tax rate, portfolio allocation). Full methodology, risks, and limitations are available upon request.

Past performance is not indicative of future results. This message should not be construed as individualized investment, tax, or legal advice, and all information is provided “as-is,” without warranty.

The material and discussions are for informational purposes only. These do not constitute investment advice and are not intended as an endorsement for any specific investment.

The information presented in this blog is the opinion of Simplify Wealth Planning and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.

We recommend consulting with your independent legal, tax, and financial advisors before making any decisions based on the information in this blog or any of the resources we provide herein (models, etc.).