Hundreds of Steps, Every Year: What You're Actually Paying For With a Financial Advisor

- Marcel Miu, CFA, CFP®

- Mar 28

- 15 min read

Updated: Apr 27

TL;DR

Most people think financial planning is about picking investments and making a plan. The actual work is a calendar of hundreds of execution steps that repeat every year. Each one has a specific sequence, a specific form, and a specific deadline. You do most of them once a year, which means you never get good at them. You're re-learning the process from scratch every year. The value proposition in handing these duties off is the tedious, deadline-driven doing that turns a plan into actual results, and the systems required to make sure none of it slips through the cracks.

The Week We Counted Everything

Recently, we sat down and tried to answer a question that had been nagging at us. We knew the work we did for clients was substantial. We knew the calendar was dense. But we'd never actually counted it all in one place.

So we mapped it. Every execution step across a typical client's financial plan. Retirement account contributions and conversions. Tax-loss harvesting. Roth conversion analysis. Beneficiary audits. Estate coordination. Insurance reviews. Estimated tax payments. Equity compensation deadlines. Trust funding.

The number came to over a couple of hundred steps.

Not concepts or ideas. Not "things to think about." Hundreds of individual steps, each with a specific order, many with hard deadlines, and many of which repeat every single year. We'd known the workload was heavy. Seeing it as a number on a page was something else.

That exercise changed how we talk about what we do. Because the truth is, a lot of the value we provide lives in the execution layer underneath the plans we build. The filing, the coordinating, the monitoring, the re-executing the following year, and the year after that. If people found that kind of work to be exciting, we'd have far fewer clients. But they hire us because that work has to get done, it has to get done right, and they've figured out (or they're about to figure out) that doing it themselves, once a year, from memory, while running the rest of their lives, doesn't actually work.

Building systems to execute all of these steps requires stitching together financial planning software, custodian portals, CRM workflows, document management, shared checklists, and calendar reminders. The infrastructure behind reliable execution doesn't appear overnight. It's the product of years of iteration, process documentation, and learning where the cracks form. Virtually every time we onboard a new client, that system catches things that a solo person doing their own finances would miss. Not because they're careless. Because they don't have a system at all.

The Part of Financial Planning Nobody Talks About

Building a financial plan matters. So does managing a portfolio, developing a tax strategy, and adjusting the approach as your life changes. All of that is real value.

But underneath all of it is an execution layer that most people never see. And it's enormous.

The way to think about it is two layers of value. Layer one is the stuff people expect when they hire an advisor. The plan, the portfolio, and the strategy. Layer two is the stuff they don't expect. The annual backdoor Roth sequence has to happen in a specific order. The beneficiary designations that need to be audited every few years and updated after every life event. The Roth conversion that has to be sized correctly against your tax bracket, your IRMAA exposure, and your estimated tax payments, all before December 31. The trust that needs assets retitled into it, or it provides no probate protection at all.

Both layers are compound. But most people only evaluate their decision to work with an advisor on layer one (strategy). And that's a mistake. In my view, the execution layer is just as valuable as the strategy layer.

Here's the thing about layer two (execution). Because we do these tasks for many clients, repeatedly, throughout the year, we've built internal systems for every one of them:

Custodian integrations

Financial planning software that flags when a deadline is approaching, or a threshold is about to be crossed

Calendared checklists for every recurring task

Documentation protocols that create a paper trail in case the IRS asks questions three years from now.

The steps are second nature because we've done them many times. Not because the steps are different, but because we don't have to re-learn them every January. The systems do what systems are supposed to do. They turn a complicated, error-prone process into a repeatable, reliable one.

Consistency is the Bottleneck

Ability isn't the bottleneck. Consistency is.

As mentioned, you will do each of these financial planning tasks once a year. That's not enough repetition to build real fluency with any of them. Procedural skills require repeated practice to stick.

Here's how it usually plays out: You know you need to do your backdoor Roth contribution before April 15. You read a blog post about it in February. You bookmark it. You tell yourself you'll handle it over the weekend. April 10 comes around, and you realize you never checked whether your old rollover IRA from a previous employer creates a pro-rata problem (if you even know to look for that). Now you have five days to figure out whether you need to roll those pre-tax dollars into your current 401(k) first. Your employer's plan administrator takes three to five business days to process incoming rollovers. You missed the deadline. That year's tax-free Roth growth is gone.

The reason this slips is that you're re-deriving the entire process from scratch while also doing your actual job, managing your household, and dealing with whatever else life threw at you that month. We aren't re-deriving anything. The execution is routine. The difference between "it got done" and "I'll get to it next weekend" is almost always the presence or absence of a system.

Vanguard estimates that outsourcing financial management saves households more than 100 hours per year. But the real cost is the mental load of keeping all of this in your head, remembering what's due when, and re-learning each process from scratch every year because you only do it once.

This communication is for informational purposes only and is not intended as tax, accounting, or legal advice. The material and discussions do not constitute investment advice and are not intended as an endorsement for any specific investment. All investments involve risk and, unless otherwise stated, are not guaranteed.

What Happens If I Get One of These Steps Wrong?

Depending on the task, you lose the benefit for a full year, you pay a penalty, or you create a tax liability that didn't need to exist. Some of these mistakes are expensive.

A few examples will help you feel the weight of what's involved.

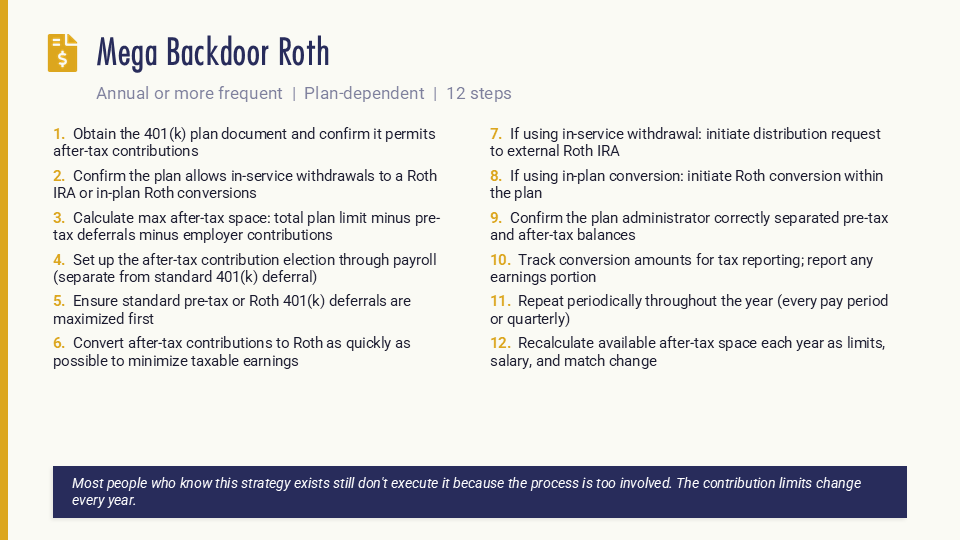

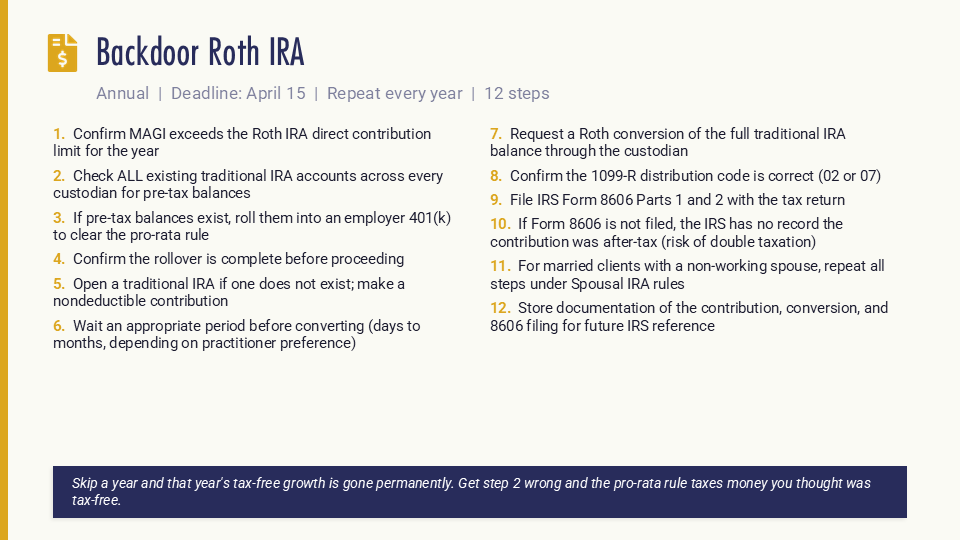

The Backdoor Roth IRA: 12 Steps That Trip People Up Every Year

The backdoor Roth is the poster child for execution complexity hiding behind a simple concept. The concept is easy: make a nondeductible IRA contribution, then convert it to Roth. Two sentences. But twelve steps.

The trap most people fall into is the pro-rata rule. If you have any pre-tax traditional IRA balance anywhere, even a forgotten rollover from a job eight years ago, the IRS doesn't let you just convert the after-tax portion. It looks at all of your traditional IRAs combined and taxes the conversion proportionally. So if 70% of your total IRA balances are pre-tax, 70% of your conversion is taxable. You can't choose to convert only the after-tax piece.

The fix requires rolling those pre-tax IRA dollars into your employer's 401(k) plan before you convert. That's a separate process with its own timeline, its own paperwork, and a plan administrator who may or may not handle incoming rollovers. All of this has to happen before April 15.

Then there's Form 8606. Both Part 1 and Part 2 must be filed with your tax return. If it isn't filed, the IRS has no record that the contribution was after-tax money. You risk being taxed again on dollars you already paid tax on (paying double taxes is about the worst outcome you could imagine, and it happens often).

And this whole sequence repeats every year. For both spouses if you're married.

Our system tracks every client's IRA landscape at the start of each year, flags any pre-tax balances that need to be cleared, initiates the contribution and conversion in sequence, confirms the custodian processed everything, and generates the documentation needed for Form 8606. The system exists because we built it by doing this for many clients simultaneously.

The backdoor Roth is just one example. The slides below show you that the multi-step execution is commonplace.

The steps shown are for educational purposes and represent general processes. The specific steps, sequence, and applicability vary by individual circumstances. Not all strategies are appropriate for every client. Consult with a qualified financial advisor before implementing any strategy.

Irreversible Consequences Are More Common Than You Think

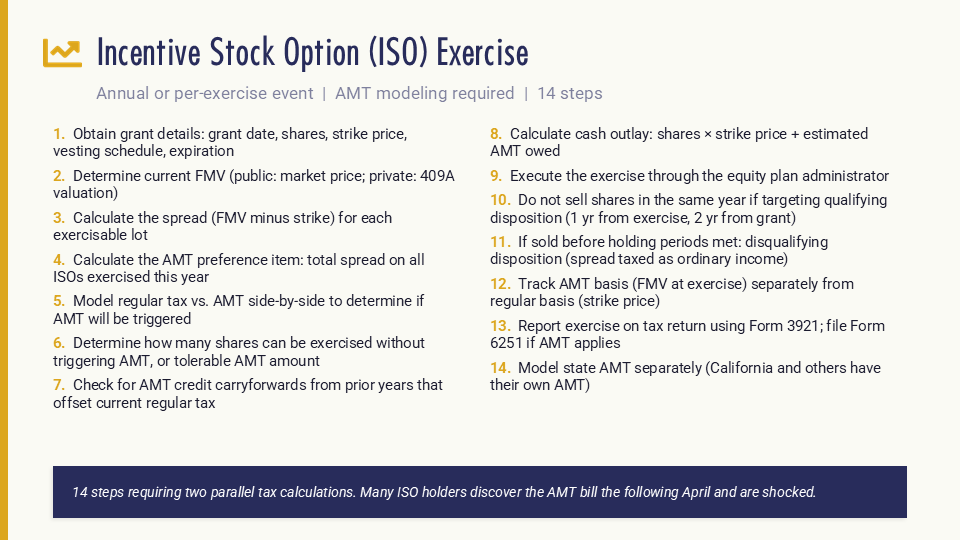

Missed deadlines in financial planning don't usually come with a second chance. An industry study in 2025 from Carta found that 67% of in-the-money employee stock options expire each year without the holder taking action. Not because those people don't want the money (they are "in-the-money" after all, meaning they technically have value). Because the decision process is complex, the tax implications are intimidating, and the steps are tedious enough that they keep getting pushed to next week until the deadline passes.

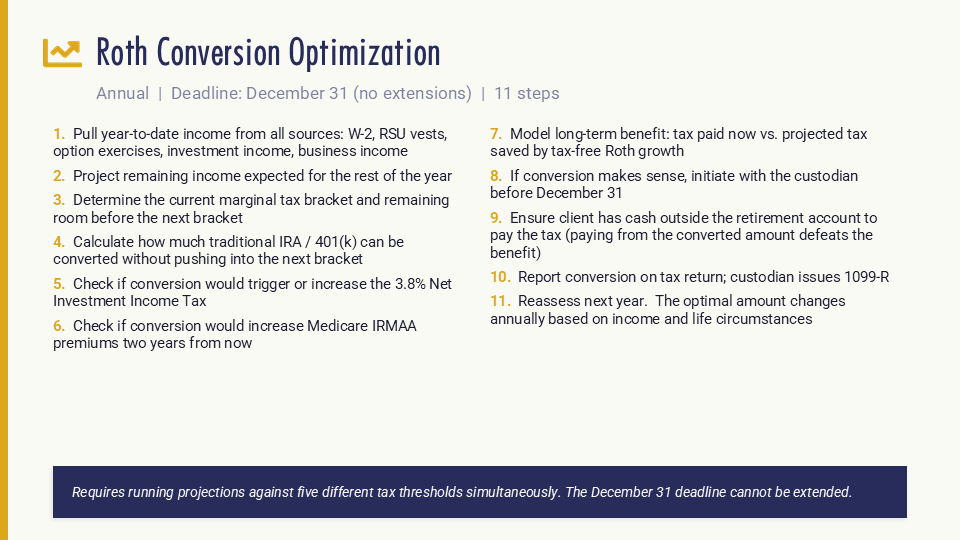

A Roth conversion that doesn't happen before December 31 can't be done retroactively. A backdoor Roth contribution missed by April 15 means that year's tax-free growth is forfeited. A trust that was signed by an attorney but never funded (no assets retitled into it) provides zero probate avoidance.

The common thread across all of these is that the consequences are permanent and the tasks are easy to defer. A system that tracks deadlines, assigns tasks, confirms completion, and follows up on loose ends is the only reliable way to make sure none of these fall through the cracks across a full year of overlapping obligations.

If I Can Google It, Why Should I Pay An Advisor?

You're paying for three things that information alone can't provide.

First, accountability. As we've mentioned, someone who makes sure it gets done, on time, every year, without you having to remember. We have systems that track these tasks to completion. You have good intentions.

Second, judgment. Someone who knows that the general answer doesn't apply to your situation because your spouse has a SEP IRA that creates a pro-rata issue, or your benefits plan changed its after-tax contribution rules last quarter, or your estate attorney set up a trust that you haven't retitled your accounts into yet.

Third, coordination. Your CPA, your estate attorney, your insurance broker, and your employer's benefits department each own a piece of your financial life. None of them talks to each other. The advisory team is the only party sitting at the center, coordinating across every domain in real time.

That third piece, the cross-domain coordination, is where the stakes are highest. A Roth conversion interacts with your tax bracket, which interacts with your income for the year, which interacts with your Medicare IRMAA premiums two years from now, which interacts with your ACA premium tax credits if you're in an early retirement gap year. One move touches four domains. No single professional outside your advisory team is tracking all of them together.

We've Already Vetted the Specialists You'd Spend Months Finding

Coordination isn't just about making sure your existing professionals are on the same page. Sometimes a situation calls for a specialist you don't have yet. A tax attorney to provide a formal opinion on a high-stakes, ambiguous tax matter. An estate planning attorney when your needs go beyond the scope of a lower-cost online solution. A property and casualty specialist when your assets require coverage that a standard homeowner's policy doesn't handle.

When those moments come up, most people start from zero. They ask friends for referrals, read online reviews, make a few exploratory calls, try to evaluate whether the person is competent and fairly priced, and hope for the best. That process alone can take weeks. And if the person they find turns out to be the wrong fit, they start over.

We maintain a vetted roster of professionals across tax, legal, insurance, and other specialties. These are people we've worked alongside on real client situations, whose work product we've seen, and whose judgment we trust. When a client's situation calls for outside expertise, we don't hand them a name and wish them luck. We make the introduction, provide context so the specialist isn't starting from scratch, and stay involved to make sure the recommendations get coordinated back into the broader financial plan.

Simplify Wealth Planning is not affiliated with, nor does it receive compensation from, third-party professionals we may recommend. We recommend consulting with your independent legal, tax, and financial advisors before making any decisions.

The judgment call of when to bring in a specialist matters as much as who to bring in. Not every tax question needs a tax attorney. Not every estate plan needs a high-end trusts and estates attorney. Part of the value we provide is knowing the difference and steering clients toward the right level of expertise for their specific situation, so they're not overpaying for a simple need or underserved on a complex one. That judgment comes from years of being in the trenches, seeing which situations truly require outside expertise and which ones don't.

What people are actually buying when they hire an advisory team, whether they frame it this way or not, is reduced regret on decisions that are high-stakes, complex, irreversible, and cross-domain. These aren't "oops, I'll fix it next year" situations. The stakes are real, the consequences stick, and the decision sits at the intersection of tax law, investment strategy, estate planning, and benefits coordination. No single Google search or AI prompt covers that intersection.

What About the Stuff That Happens Every Single Day?

Not all execution work is annual. Some of it runs daily.

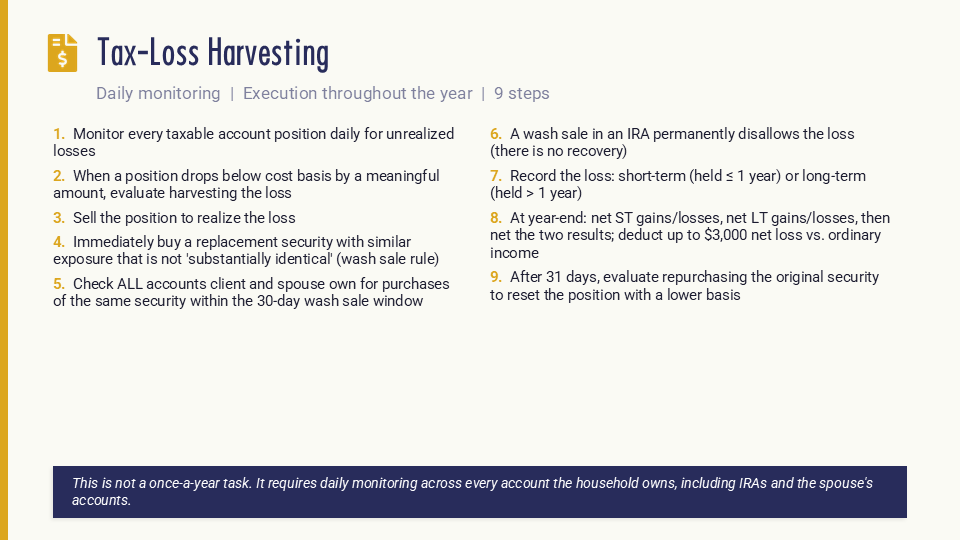

Tax-loss harvesting is the clearest example. It requires monitoring every position in every taxable account the household owns, every day, looking for unrealized losses worth harvesting. When a position drops below its cost basis, you sell it, immediately buy a replacement security that isn't "substantially identical" (to avoid the wash sale rule), and track the 30-day window across all accounts. That includes the spouse's accounts. That includes IRAs.

The steps themselves aren't complicated. But the discipline of checking every position in every account every day is not something any normal person builds into their morning routine. This is where purpose-built systems matter most. Our team monitors this through software that flags opportunities as they arise. The process runs in the background, across all client households, every market day. For a DIY investor, it runs whenever they remember to check, which in practice means it doesn't run at all. (Tax-loss harvesting can reduce your tax bill, but it doesn't eliminate taxes entirely, and the benefit depends on your individual tax situation, the size of your portfolio, and market conditions.)

None of this happens in isolation, either. The losses you harvest interact with capital gains from stock sales, which interact with Roth conversion bracket math, which interact with estimated tax payments, which interact with ACA premium tax credits if you're in an early retirement gap year. One move touches four domains. Again, the advisory team is the only party coordinating across every domain in real time.

What Does the Full Year Actually Look Like?

It's a 12-month calendar of overlapping deadlines, and it resets every January.

January starts with setting contribution elections for the 401(k), HSA, and any after-tax contribution strategies. The annual cash flow projection gets updated.

By March 15, certain business entity deadlines have passed for clients with side businesses. The backdoor Roth contribution for the prior year needs to be in process.

April 15 brings the prior-year IRA contribution deadline, the first quarterly estimated tax payment, and the tax return itself, which includes Form 8606 for anyone who did a backdoor Roth.

The summer months are for mid-year tax projections, Roth conversion analysis, and portfolio rebalancing. Second and third quarter estimated tax payments land in June and September.

October through December is the most compressed window. Roth conversions must be completed by December 31. RMDs must be processed. Tax-loss harvesting gets a final review. Charitable giving strategies need to be executed. Open enrollment for health insurance and employer benefits happens in this window.

January 15 brings the fourth quarter estimated tax payment.

Then it starts over.

You're managing a schedule of dozens of interlocking tasks across retirement accounts, tax strategy, insurance, estate planning, and investment management. Simultaneously. While doing your actual job.

Our internal system tracks every one of these deadlines for every client. That system is the reason things get done in February instead of getting remembered in May.

The tax and estate planning information offered is general in nature and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. There are no assurances that any financial strategy will be successful.

What's the Real Value In Working With An Advisor?

It comes from everywhere. The plan itself. The portfolio management. The tax strategy. The behavioral coaching during market downturns. And the execution layer that makes all of those things actually happen on time, every year, without anything falling through the cracks.

Vanguard's Advisor's Alpha study estimated approximately 3% in net returns for clients who work with an advisor, though the firm notes the actual figure can vary widely depending on the client and the year. Their framework breaks the value into components: lower expense ratios, rebalancing, asset allocation, withdrawal sequencing in retirement, and behavioral coaching. That last component, behavioral coaching, accounted for roughly 1.50% on its own, reflecting the value of keeping people from selling at market bottoms and chasing performance at market tops.

Even that framework doesn't fully capture the execution layer. It doesn't measure the backdoor Roth that got done on time. It doesn't measure the beneficiary designation that got updated before it was too late. It doesn't measure the trust that actually got funded with assets instead of sitting as an empty legal document. And it doesn't measure the value of having a vetted tax attorney on speed dial when a complex situation requires a formal opinion, instead of spending weeks searching for one from scratch.

The combined value of strategy, plus execution, plus systems-driven efficiency is what makes the advisory relationship worthwhile for most people in this situation.

(Every client's circumstances are different, past results don't guarantee future outcomes, and the specific value depends on your financial complexity, discipline, and goals.)

FAQs

Can't I automate most of this with software?

Some things can be partially automated. Daily tax-loss harvesting, for example, runs through software that monitors positions and flags opportunities. But the backdoor Roth process, coordination with your employer on after-tax contributions, Roth conversion bracket analysis, RMD calculations on inherited IRAs, trust funding, and beneficiary audits all require human judgment, coordination with third parties, and manual execution. Software helps. It doesn't replace the person using it or the system around it.

I already have a CPA. Isn't that enough?

A CPA prepares your tax return. They report what happened. An advisory team makes things happen before the tax return is filed: the Roth conversion in the right amount, the tax-loss harvest in the right account, and the beneficiary update before a life event creates a problem. By the time your CPA sees your documents, the execution window for most of these strategies has already closed.

What if I only need help with one thing, like my backdoor Roth?

In my experience, one thing is never one thing. The backdoor Roth interacts with the pro-rata rule (all your IRA balances), your tax bracket (which affects whether a Roth conversion even makes sense this year), your spouse's IRA situation, and Form 8606 on your tax return. Pulling one thread affects others.

What if I miss one of these deadlines?

Depends on the deadline. Miss a backdoor Roth contribution by April 15? That year's tax-free growth opportunity is lost. Miss an RMD? 25% penalty on the amount not withdrawn. Miss the window to fund a trust with a newly purchased asset? That asset goes through probate. Some deadlines are recoverable. Many aren't.

I'm financially literate. Do I really need someone?

Financial literacy and execution are different skills. You probably understand the concept of a backdoor Roth, tax-loss harvesting, and Roth conversions perfectly well. Whether you'll actually complete all of them, in the right sequence, by the right deadline, while also coordinating with your CPA, your estate attorney, and various plan administrators, is a different question entirely. High earners aren't paying for education. They're paying for coordination, accountability, and a system that ensures the kind of mistakes that are expensive and permanent don't happen.

The Plan Doesn't Execute Itself

The value of an advisory team isn't only in the plan or the portfolio. A plan is a document. A portfolio is a collection of holdings. The real value is in the hundreds of steps that turn both of them into actual dollars saved, actual forms filed, actual deadlines met, and actual money that didn't get left on the table. The plan, the investments, and the execution all matter. But the execution is the part that falls apart when you try to do it alone, once a year, while running the rest of your life.

You're paying for the system behind the person. The calendars, the checklists, the software, the documentation, the follow-up, the vetted network of specialists ready to be called in when your situation demands it.

We built our practice around all three layers: strategy, investment management, and execution. And because we do the execution work every day, across many clients, with systems designed for exactly this, we do it in a fraction of the time it would take you.

If you want to see what a full year of financial planning execution looks like for someone in your situation, schedule an introductory call to learn more about our approach and whether it's a good fit for your needs.

To learn more about how we partner with clients, click here to view our services.

This blog is for educational purposes only and should not be taken as individual advice

Simplify Wealth Planning

Fast-Tracking Work Optional For Employees Earning Company Stock | Turn Your Stock Comp Into Wealth, Cut Taxes & Live Life Your Way | Flat Fees Starting at $8,000

Marcel Miu, CFA and CFP®, is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping employees earning company stock master their money and achieve their financial goals.

Disclosures

Simplify Wealth Planning, LLC (“SWP”) is a registered investment adviser in Texas and in other jurisdictions where exempt; registration does not imply a certain level of skill or training.

If this blog refers to any client scenario, case study, projection, or other illustrative figure, such examples are hypothetical and based on composite client situations. Results are for informational purposes only, are not guarantees of future outcomes, and rely on assumptions specific to the scenario (e.g., age, time horizon, tax rate, portfolio allocation). Full methodology, risks, and limitations are available upon request.

Past performance is not indicative of future results. This message should not be construed as individualized investment, tax, or legal advice, and all information is provided “as-is,” without warranty.

The material and discussions are for informational purposes only. These do not constitute investment advice and are not intended as an endorsement for any specific investment.

The information presented in this blog is the opinion of Simplify Wealth Planning and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.

We recommend consulting with your independent legal, tax, and financial advisors before making any decisions based on the information from this blog or any of the resources we provide herewithin (models, etc).