When Should You Claim Social Security to Maximize Lifetime Value?

- Marcel Miu, CFA, CFP®

- May 30

- 8 min read

Summary

Claiming Social Security is not a simple math equation aimed at hitting a breakeven age. It functions as your baseline longevity insurance. Claiming at age 62 provides immediate cash flow but permanently reduces your monthly payout. Delaying until age 70 offers an eight percent annual step-up in benefits under current rules. High earners must weigh the tax torpedo, the earnings test, and the costs of bridging the gap with portfolio assets. All strategies carry risk, including legislative changes to the program and outliving your investment portfolio.

The Longevity Gamble: Beyond the Breakeven Point

Let's imagine a professional looking to wrap up a career in the corporate world. He wants to claim Social Security at age 62. He ran a breakeven analysis to see how long he needed to live to make delaying until age 70 worthwhile. The math showed the total payouts crossing near age 80. He assumed he wouldn't live past 80, so he decided to take the money early.

That approach ignores a major financial risk. The real danger in retirement is not dying early and leaving money on the table. The risk is living to age 95 and depleting your portfolio. A breakeven analysis should focus on the right timeline: modeling the tail risk of extreme old age. Social Security provides a rare inflation-adjusted income stream that lasts as long as you do.

Early retirees often benefit from using other bridge strategies to fund their lifestyle while letting their government benefits grow. Such as drawing from taxable accounts or strategic retirement distributions to provide the cash you need today. This gives your Social Security benefit time to maximize. But it's not so simple. There's always a risk that drawing down personal assets early could deplete them if markets decline. So, you must weigh the guaranteed benefit growth of waiting to claim Social Security against market volatility in your investment portfolio.

How Is Your Social Security Benefit Actually Calculated?

The government does not simply look at your last paycheck. The Social Security Administration calculates your Primary Insurance Amount using your Average Indexed Monthly Earnings. They take your 35 highest-earning years and index them to wage inflation. If you worked fewer than 35 years, they plug in zeros for the missing years. Those zeros can drag down your average significantly.

The system uses bend points to keep things progressive. High earners eventually see diminishing returns on their payroll taxes. The formula replaces a large percentage of your first chunk of income but a much smaller percentage of your highest earnings.

You reach your Full Retirement Age between 66 and 67, depending on your birth year. Claiming at age 62 results in a permanent reduction of up to 30 percent of your baseline benefit. Delaying past your Full Retirement Age earns you delayed retirement credits. Under the current law, your benefit grows by eight percent per year up to age 70. The federal government backs this growth, though future funding shortages could lead to benefit cuts.

What Are You Really Optimizing For?

The Breakeven Fallacy vs Longevity Risk

Most people start with the breakeven calculation. They compare the total cash received by claiming early versus delaying. The math usually shows the lines crossing in your late 70s or early 80s. This logic breaks down when you consider extreme old age.

Living past age 90 is increasingly common. At that stage, your investment portfolio might be stretched thin from decades of withdrawals and market cycles. A maximized Social Security benefit protects against that scenario. But delaying means you spend down your portfolio faster in your 60s. This early spending exposes you to a sequence of returns risk if the market drops early in retirement. So, you have to balance the security of a higher lifetime payout against the depletion of your liquid assets.

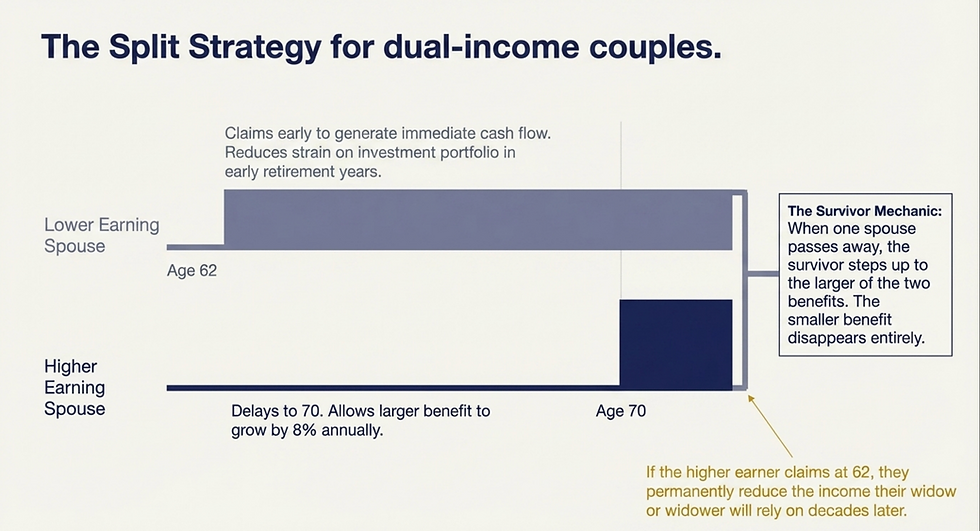

The Split Strategy for Married Couples

Dual-income couples have more options to manage their cash flow. The split strategy involves the lower-earning spouse claiming benefits early while the higher-earning spouse delays until age 70.

This generates immediate cash flow to help cover daily expenses. It also reduces the strain on your investment portfolio in the early years of retirement. Meanwhile, the higher earner lets their larger benefit grow by eight percent annually. This requires careful planning. Claiming early permanently reduces the lower earners' benefit.

Optimizing for Survivor Protection

Survivor benefits are a massive factor for married couples. When one spouse passes away, the surviving spouse steps up to the larger of the two benefits.

Maximizing the higher earners' benefit locks in a safety net for the surviving spouse. If the higher earner claims at 62, they permanently reduce the income their widow or widower will rely on decades later. Delaying can protect the survivor.

How Do Taxes Impact Your Social Security Benefits?

The Tax Torpedo and Provisional Income

People often face a rude awakening when they realize their Social Security benefits are taxable. The IRS uses a formula called Provisional Income to determine how much of your benefit falls subject to federal income tax.

Provisional Income equals your Modified Adjusted Gross Income plus half of your Social Security benefit. If you file as a single taxpayer and your Provisional Income exceeds $34,000, up to 85 percent of your benefit becomes taxable. Married couples filing jointly hit that 85 percent threshold at $44,000. These thresholds are not adjusted for inflation.

This creates the tax torpedo. Earning just a little extra income from portfolio withdrawals or a part-time job can push your Social Security benefits into the taxable bracket. This effectively spikes your marginal tax rate.

High-income events trigger the torpedo. Major events like large portfolio withdrawals can drastically spike your Modified Adjusted Gross Income. This pushes Provisional Income well over the limits, and likely results in 85 percent of your benefits being subject to federal income tax that year.

The Hidden Roth Strategy and the Senior Deduction Window

You can proactively plan for the tax torpedo. The period between retiring early and taking Required Minimum Distributions in your 70s offers a unique tax planning window.

During these gap years, your taxable income often drops significantly. You can use this low-income phase to execute strategic Roth conversions. Converting pre-tax money to a Roth IRA requires paying ordinary income taxes today. You do this at a potentially lower bracket than you will face later. Once funds are in a Roth IRA, qualified distributions are tax-free. They do not count toward your Provisional Income.

Keeping your taxable income low in retirement requires acting before you are forced to take distributions. Roth conversions carry risks, including the possibility that tax rates decrease in the future or that paying the conversion taxes depletes your liquid assets.

Key Takeaways

Social Security acts as inflation-adjusted longevity insurance rather than a standard investment.

The Primary Insurance Amount relies on your 35 highest earning years.

Claiming at age 62 permanently reduces your monthly payout, while delaying to 70 guarantees an eight percent annual step up under current law.

Optimizing for the highest lifetime value can protect you against depleting your portfolio in extreme old age.

The split strategy provides early liquidity for dual-income couples while maximizing survivor benefits.

Provisional Income thresholds push up to 85 percent of your benefits into taxable territory for high earners.

Strategic Roth conversions during early retirement can help reduce your future tax burden and avoid the tax torpedo.

FAQs

Will Social Security run out before I retire?

The system is funded by ongoing payroll taxes, meaning it will not completely run out of money. However, the trust funds that support full payments face depletion over the next decade. If Congress does not act, future benefits could see an across-the-board reduction.

Can I change my mind after I start claiming my benefits?

Yes. You get one opportunity to withdraw your application within 12 months of claiming. You must repay all the benefits you and your family received. After that, you can suspend your benefits once you reach Full Retirement Age to earn delayed retirement credits.

Your Next Steps

Pull your Social Security statements. Download your exact earnings record from the Social Security Administration website to verify your history.

Evaluate your bridging assets. Identify which taxable accounts, vested equity, or early withdrawal strategies can sustain your lifestyle while you delay claiming.

Coordinate with your spouse. Map out the age gap and earnings gap between you and your partner to determine if a split strategy makes sense.

Run a tax projection. Calculate your anticipated Provisional Income to see how heavily your benefits will be taxed upon claiming.

Securing Your Retirement Income Strategy

Claiming Social Security is a massive and largely irrevocable decision. It integrates tightly with your portfolio withdrawals, your tax liability, and your estate plan. There is no one-size-fits-all math equation. Every choice carries tradeoffs between immediate cash flow and long-term security.

Tired of guessing how it all fits together? Let's talk about building a plan designed for long-term tax efficiency.

Schedule your introductory call today to learn more about our approach and determine if our services are a good fit for you.

To learn more about how we partner with clients, click here to view our services.

This blog is for educational purposes only and should not be taken as individual advice

Simplify Wealth Planning

Fast-Tracking Work Optional For Employees Earning Company Stock | Turn Your Stock Comp Into Wealth, Cut Taxes & Live Life Your Way | Flat Fees Starting at $9,000

Marcel Miu, CFA and CFP®, is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping employees earning company stock master their money and achieve their financial goals.

Disclosures

Simplify Wealth Planning, LLC (“SWP”) is a registered investment adviser in Texas and in other jurisdictions where exempt; registration does not imply a certain level of skill or training.

If this blog refers to any client scenario, case study, projection, or other illustrative figure, such examples are hypothetical and based on composite client situations. Results are for informational purposes only, are not guarantees of future outcomes, and rely on assumptions specific to the scenario (e.g., age, time horizon, tax rate, portfolio allocation). Full methodology, risks, and limitations are available upon request.

Past performance is not indicative of future results. This message should not be construed as individualized investment, tax, or legal advice, and all information is provided “as-is,” without warranty.

The material and discussions are for informational purposes only. These do not constitute investment advice and are not intended as an endorsement for any specific investment.

The information presented in this blog is the opinion of Simplify Wealth Planning and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.

We recommend consulting with your independent legal, tax, and financial advisors before making any decisions based on the information in this blog or any of the resources we provide herein (models, etc.).